The Myth Busting Economist by Larry Malone

Spending, Deficit Kerfuffle Examined

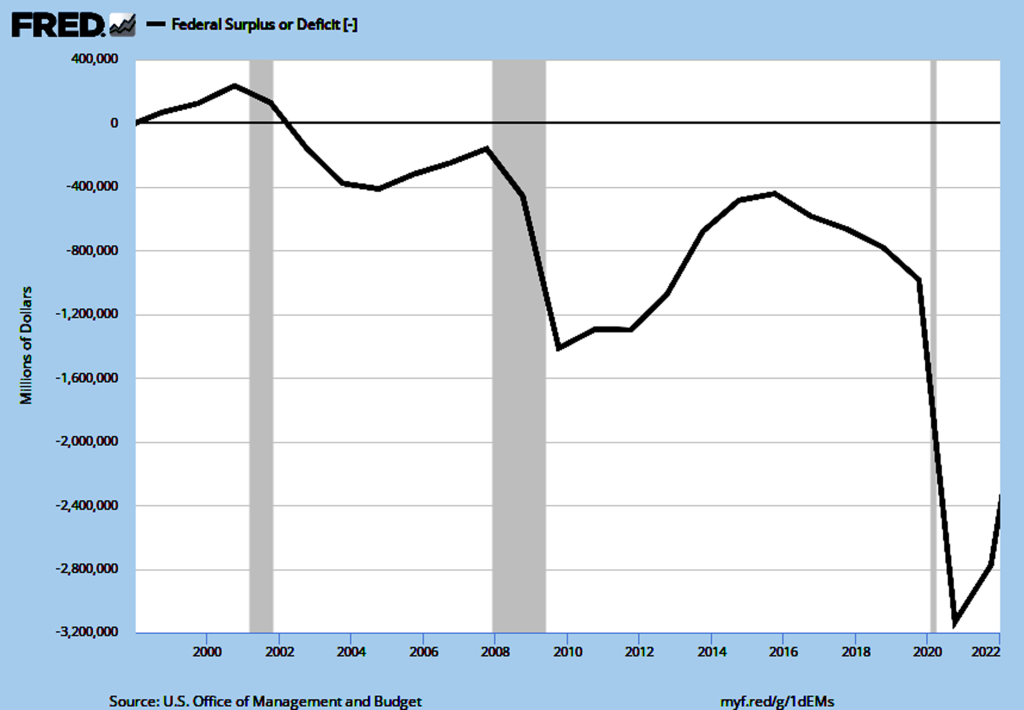

Some of us would like national health care, while others want to cut Social Security. We take up federal government spending in this column, but we’ll stay away from what it buys. Our myth busting will instead clarify the relationship between federal spending and budget deficits, and show where the deficits came from.

As I wrote these words, another federal government shutdown was looming. The January 19 deadline was part of a “kick the can down the road” deal in November to provide enough funds to keep the government running for another 65 days. That meant veterans would still receive benefits, people could visit the Grand Canyon and farmers would get their subsidies.